Androscoggin’s Wealth Building Home Loan

Androscoggin Bank of Lewiston, ME introduced the first market rate program Wealth Building Home Loan with a soft launch back in November (called the Wealth Builder Home Loan). The response has been enthusiastic—5 closed loans and a total pipeline (including closed loans) of $3.3 million in the dead of winter—impressive results for a $700 million asset bank. The bank had its formal launch on February 4 (see attached PowerPoint for more detail). The bank added an innovative feature–a 15 year 2-step loan with the bought down rate fixed for 7 years and then stepping up to a pre-set rate for the remaining term (described in detail below).

Also see https://www.androscogginbank.com/Personal/Loans/Mortgage/Wealth-Builder. The February 4 event was attended by about 40 realtors and the bank described the response as “unprecedented” —92% and 8% of attendees said they would be either be “very likely” or “likely” to recommend to their clients (see realtor survey results attached).

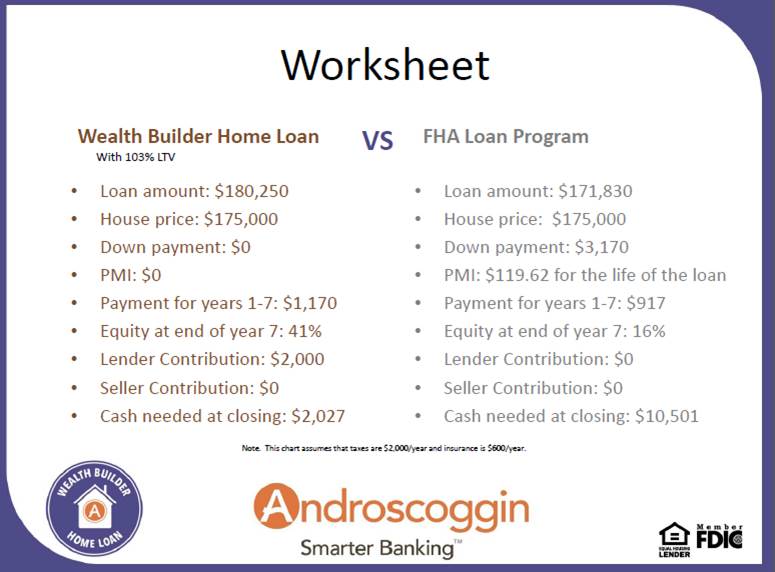

The bank also offers a 103% LTV 15 year loan that minimizes the cash needed at closing, while still greatly reducing default risk (see worksheet below).

For a larger view click on the image.

The chart below compares an FHA loan (96.5% loan + upfront fee, with 0.80% annual MIP) to Androscoggin Bank’s 100% LTV and two-step 15-year loan (no MI). Home price of $100,000 used for simplicity:

| FHA

30 year*

|

Androscoggin

15 year 2-step** |

|

| Rate/P&I (inc. MIP for FHA) on $100,000 | 4%/$535 | 1.75%/$632 |

| Pre-tax annual income/buying power vs. FHA | $27,374/100% | $29,449/93% |

| Net equity after 7 years (10% selling expenses, 2% annual appreciation) | $18,828 | $46,798 |

| 90% LTV reached in month? | 54 | 21 |

| 80% LTV reached in month? | 108 | 40 |

| Payment shock (year 8) | NA | 13.3% (1.9% per yr.) |

*96.5% LTV + upfront fee, with 0.80% annual MIP. No use of residual income, based on 28% housing debt-to-income

**100% LTV plus 3 buydown points. Rate fixed for years 1-7, steps to 5% for years 8-15. Use of residual income allows for 2% higher housing debt-to-income (30%).

In this next chart, you will see that the bank has a 100% or 103% LTV, max. 45% DTI, min. 4-6 months reserves, min. 660 FICO, and uses the residual income approach (the residual income #s are the same as used by the VA). This makes for a compelling loan offering, yet results in a much lower risk loan than with FHA.

| DTI | FICO | Reserves | LTV | Residual income $ and household size | |||||

| 1 | 2 | 3 | 4 | 5 | 6+ | ||||

| 45.00 | 660 | 4 mo. | 100 | $450 | $755 | $909 | $1025 | $1062 | $1062 |

| 45.00 | 660 | 6 mo. | 103 | $450 | $755 | $909 | $1025 | $1062 | $1062 |