The Concorde Coalition says it’s the Budget Stupid!

WASHINGTON, D.C. /PRNewswire-USNewswire/ — Sobering 30-year projections that the Congressional Budget Office (CBO) released today underscore the need for the 2016 presidential and congressional candidates to provide voters with credible plans to put the federal budget on a more responsible course, according to The Concord Coalition.

“If current laws remained generally unchanged, the United States would face steadily increasing federal budget deficits and debt over the next 30 years—reaching the highest level of debt relative to GDP ever experienced in this country” – Congressional Budget Office.

“Americans like to think we put a high priority on strengthening the country and looking out for the next generation, but the CBO’s latest long-term projections show once again that we are falling far short on both counts,” said Robert L. Bixby, Concord’s executive director. “Those who aspire to national leadership should take a good look at these projections and explain to the public how they intend to avoid the intense budget pressures and grave economic consequences toward which current policies are leading us.”

Bixby added:

“If candidates for federal office over the next few months ignore the CBO’s warnings of severe trouble ahead, whoever wins in November will not have a clear mandate for the reform measures needed to rein in the federal debt, strengthen the economy and protect our children’s future.”

The federal deficit has been dropping in recent years, creating a sense of complacency in Washington about the need for such reforms. Yet under current law the deficit is rising again this year and the debt will continually grow more quickly than the economy — a trend that is ultimately unsustainable.

Today’s CBO report looks out over the next three decades and projects even greater government debt and fiscal pressures after 2026.

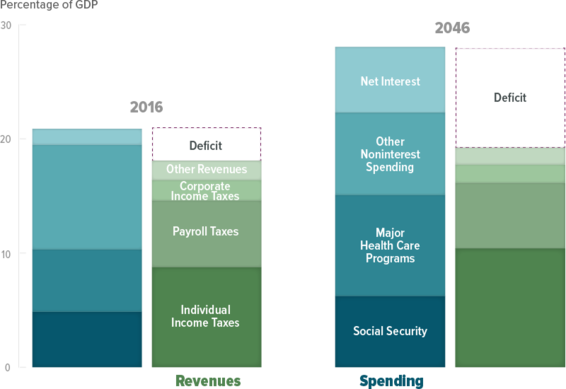

The federal debt held by the public, which was only 39 percent of GDP at the end of Fiscal 2008, has climbed to 75 percent. That is already high by historical standards. The budget office projects that under current law, that debt would rise to 86 percent of GDP in 2026 and to 141 percent in 2046 — far exceeding the historical peak of 106 percent shortly after World War II.

As the CBO points out, such high levels of public debt would reduce national savings and income, increase interest costs that would put more pressure on the rest of the budget, limit the nation’s ability to respond to unforeseen problems and increase the likelihood of a fiscal crisis in which investors would demand extremely high interest rates on further loans to the government.

“The changes needed to bring about a sustainable fiscal policy are substantial and the costs of delay are profound, yet so far the 2016 presidential candidates have said nothing that comes close to addressing the challenges identified in CBO’s report,” Bixby said.

According to CBO, simply keeping the debt-to-GDP ratio from rising above its current level, would require spending cuts and/or tax increases totaling 1.7 percent of GDP in every year through 2046. That would amount to $330 billion in 2017.

Waiting until 2022 would require annual changes totaling 2.1 percent of GDP, and procrastinating until 2027 would require annual changes totaling 2.7 percent of GDP.

The choice about when to make policy decisions also has different generational impacts. As CBO says: “Reducing deficits sooner would probably require today’s older workers and retirees to sacrifice more and would benefit today’s younger workers and future generations. By contrast, reducing deficits later would require smaller sacrifices by older people and greater sacrifices by younger workers and future generations.”

An aging population and rising health care costs are key factors in the government’s growing financial problems. As more people retire, the government must spend more just to maintain current levels of service. Health care costs rise as more treatments become available and demand for them increases.

CBO says federal spending on Social Security, the government’s major health problems and other “mandatory” programs would rise from 13.2 percent of GDP today to nearly 16.9 percent in the decade starting in 2037.

The budget office also warns that interest payments on the federal debt are expected to rise rapidly as government borrowing continues and low interest rates return to normal levels. Net interest costs now amount to only 1.4 percent of GDP but that figure is expected to rise to 5.1 percent after 2037.

The CBO report shows other areas in the federal budget — even those that may prove critical to the nation’s future — being squeezed harder and harder in the coming years. CBO projects that over the next 30 years spending on national defense, infrastructure, research and development, and everything else other than health care, Social Security and interest payments would drop to 5.2 percent of GDP, down from 6.5 percent today.

In addition to more thoughtful spending decisions in Washington, reasonable reforms in the federal tax system could help boost the economy and reduce federal borrowing.

“As in past years, CBO’s long-term projections are a valuable reminder that the federal budget is not on a sustainable course,” Bixby said. “Interest payments and a few spending programs, no matter how important, cannot be allowed to squeeze other national priorities out of existence. Voters this year would do well to look for candidates who understand this and are prepared to do something about it.”

ABOUT THE CONCORD COALITION

The Concord Coalition is a nationwide, non-partisan, grassroots organization advocating generationally responsible fiscal policy. The Concord Coalition was founded in 1992 by the late former Senator Paul Tsongas (D-Mass.), late former Senator Warren Rudman (R-N.H.), and former U.S. Secretary of Commerce Peter Peterson. Former Senator Sam Nunn (D-GA) serves as co-chair of the Concord Coalition.

RELATED ARTICLE: The 15th Obamacare Co-Op Has Collapsed. Here’s How Much Each Failed Co-Op Got in Taxpayer-Funded Loans.